What You’ll Learn

Growth equity private equity funds focus on businesses with significant growth potential. These companies typically have established business models, a proven track record of generating cash, and are often targeted through minority stakes acquisitions.

Investors view growth equity as a middle ground between venture capital and buyout funds, reflecting the transitional stages in the lifecycle of the target companies.

Growth equity funds generally target industries such as technology, consumer goods, and healthcare, which are known for their scalability and innovation.

Over the past decade, growth equity fundraising has outpaced other private equity strategies. Despite a slowdown caused by rising interest rates and geopolitical challenges, growth equity deals regained momentum in 2023, surpassing leveraged buyout (LBO) transactions. That year, growth equity accounted for 12.7% of the total private equity deal value.1

Buyout firms are increasingly acquiring companies that have already received growth equity investments, further integrating these strategies into the broader private equity landscape.2

What Is Growth Equity?

Growth equity, also called expansion capital or growth capital, focuses on investing in companies with rapid revenue growth, undergoing transformation, and demonstrating significant potential for expansion.3

Fund managers typically acquire minority stakes in established middle-market companies, avoiding full control, and plan their exit strategies through sales, direct listings, or initial public offerings (IPOs).4

These managers, known as general partners (GPs), provide the financial resources needed to accelerate growth, aiming to achieve high returns upon exit. Investments are often structured using preferred shares, which give investors priority over common shareholders in asset claims and dividend distributions but do not confer voting rights, leaving operational control with the company's management.

Growth Equity Targets

GPs typically target companies that occupy a middle ground between early-stage firms sought by venture capitalists and mature businesses pursued for leveraged buyouts. These companies are often industry leaders with strong business models, proven products, and growing customer bases, making them attractive for growth equity investments.

GPs typically prioritize companies with rapid revenue growth, minimal or no debt, and positive cash flow, avoiding the higher risks associated with early-stage ventures. Target companies often seek external funding to drive initiatives like new product development, operational expansion, market entry, or acquisitions.

Growth equity capital frequently serves as the first institutional investment in owner-operated businesses. These firms usually maintain low debt levels and are either profitable or at least breaking even before seeking outside capital.5

The decision to sell minority stakes for growth equity capital often marks a pivotal stage in a company's lifecycle, allowing for a strategic infusion of funds.6

For businesses with steady revenue growth that are not yet profitable, minority equity financing can serve as an alternative to debt. Beyond capital, companies selling minority stakes to private equity managers often seek strategic guidance for product development, geographic expansion, and increasing market share.7

Growth Equity Emerges as PE Firms Diversify From Venture, Buyout

Growth equity has emerged as a distinct asset class within private markets, driven by private equity fund managers seeking to diversify their strategies beyond venture capital and buyouts.8

Positioned between these two investment types in terms of the developmental stage of target companies, the average growth equity fund size over the past decade has been approximately $300 million, ranging from $159 million in 2015 to $513 million in 2023.9

The expansion of this category has been fueled by various factors, with a broadened investable universe playing a pivotal role in the rise of growth equity as an asset class.10

Fundraising Environment for Growth Equity Strategies

The growing interest from limited partners in private markets, outpacing interest in publicly traded firms, has driven significant growth in private equity fundraising. This trend is also supported by an expanding pool of investable companies, fueled by venture capital investments in recent years.11

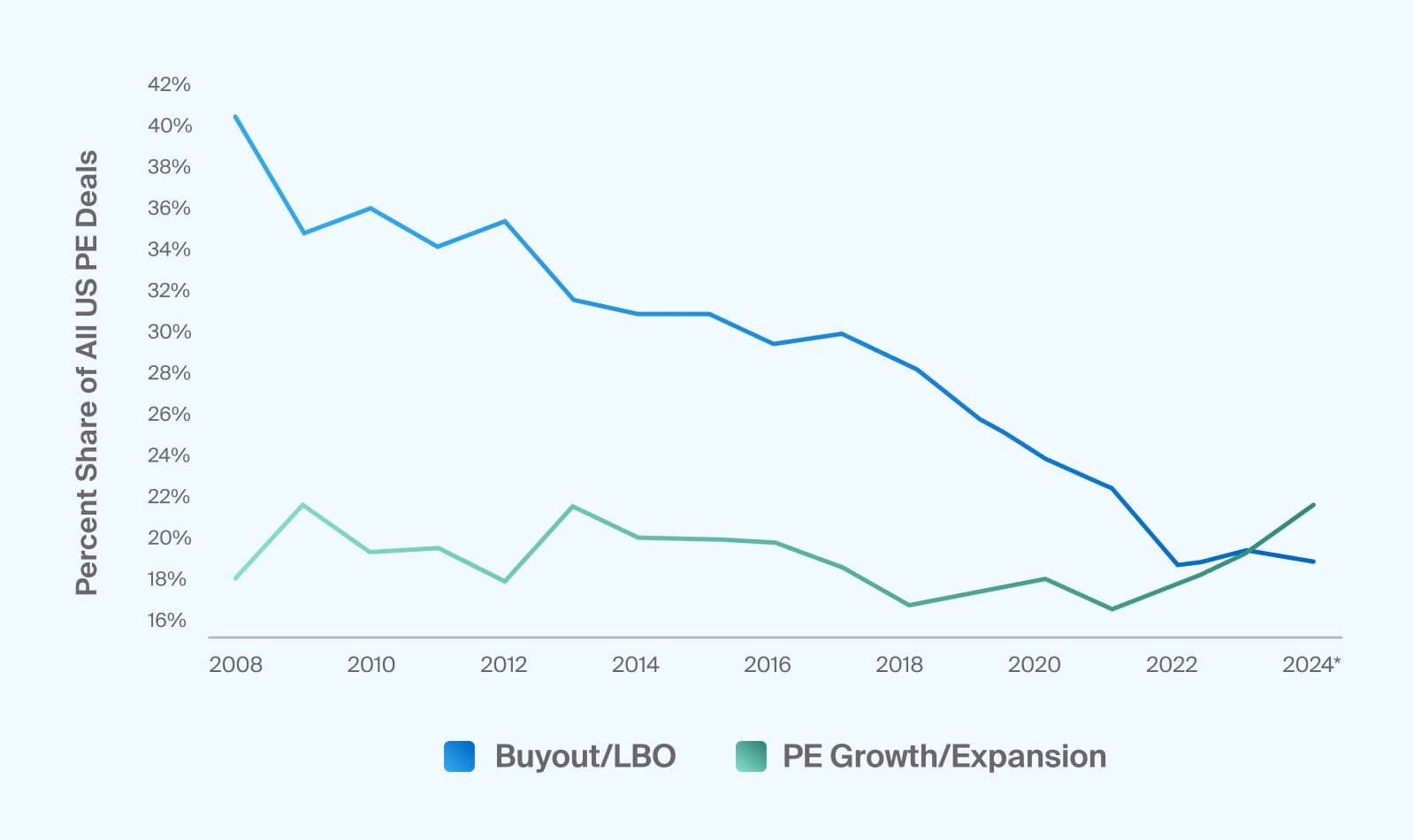

In the first half of 2024, growth equity transactions accounted for 23% of private equity deals, surpassing buyout transactions, which constituted 19% during the same period, according to Pitchbook data,12 as shown in Exhibit 1.

However, because growth equity investments typically involve minority stake acquisitions, their total dollar value remains lower, representing just 12.3% of deal value in the third quarter of 2024.

Footnotes

Source: Pitchbook's Q2 2024 US PE Breakdown, Geography: US. As of June 30, 2024

Private Equity Growth Assets Reach Nearly a Quarter of All PE Deals (Exhibit 1)

Buyout GPs have increasingly shown interest in acquiring growth-equity-backed companies as original GPs exit, driven by the substantial dry powder they have accumulated.

Fundraising activity has also accelerated as buyout private equity firms adopt hybrid deal strategies.13 These approaches allow existing private equity owners to retain investments while enabling new owners to enter at more favorable valuations.

Growth Equity Strategies’ Historical Performance

Historically, growth equity fund performance has closely resembled that of buyout and venture capital funds, according to Cambridge Associates. However, performance across these categories has varied over time in response to market conditions.

While the performance spread was more pronounced during the 1990s and early 2000s, particularly during the Dot-Com bubble, it has narrowed in recent years as the growth equity category has matured, as shown in Exhibit 2.

Footnotes

Source: Growth Equity Primer, Meketa, May 2024; Cambridge Associates via IHS Markit, annualized quarterly Pooled IRR as of September 30, 2023 (pulled in January 2024)

Growth Equity, Buyout, and Venture Capital: Similar Return Patterns (Exhibit 2)

Over the past 10- and 20-year periods in the US, growth equity has outperformed venture capital and buyout funds, delivering annualized returns of 17.2% and 15.7%, respectively, according to data from Cambridge Associates via IHS Markit.14

Growth equity can also provide diversification compared to certain public and private equity.

However, growth equity funds carry risks typical of private equity, including illiquidity and the J-curve effect, where early returns are often negative due to upfront costs and slow initial deployment of capital. These funds are also exposed to sector-specific risks and the lack of control over management decisions, which can lead to conflicts with company owners and leadership.

Growth equity investments require long holding periods, with exits dependent on stock market conditions and IPO environments. Prolonged holding periods may result in additional capital requirements if market conditions delay planned exits.

Growth Equity Risks and Considerations

The risk and return profile of growth equity funds falls between that of venture capital and buyout private equity funds. Growth equity tends to carry less risk than venture capital due to its focus on acquiring minority stakes in relatively mature, established companies.

Growth equity managers typically target companies with little to no leverage, prioritizing organic growth and strategic acquisitions over cost-reduction strategies.15

Manager selection plays a critical role in determining investment outcomes, as the performance gap between top-performing and underperforming funds can be significant.16