What You’ll Learn

Financial advisors can consider strategies like commitment pacing when targeting specific private equity allocations as a way to potentially diversify across vintages and smooth out performance dispersion across market cycles.

A private equity fund lifecycle includes fundraising, investing, and harvesting phases. Reinvesting harvested proceeds may mitigate the J-curve effect.

Evergreen funds can provide exposure to private equity, lower minimums, and limited liquidity. Evergreen funds also come with constraints like redemption fees and potential suspensions during market stress.

When combined in a potential core-satellite private equity strategy, evergreen funds can serve as the core, diversified exposure, while drawdown funds may act as satellite investments focused on growth opportunities.

As financial advisors integrate private equity into client portfolios aiming to enhance risk-return profiles,1 the complexity of managing exposures may become evident. Illiquidity, unpredictable capital calls, and long-term commitments are all features of private equity investments that a toolset can address.

With a strategic plan for pacing commitments and diversifying portfolios across fund vintages, advisors may improve their chances of avoiding suboptimal performance and cash drag—in other words, the loss of potential returns when money sits idle in cash instead of being invested. They can learn from pension funds and endowments—which rely on commitment pacing programs and vintage diversification—how to manage capital calls and smooth out performance dispersion across market cycles.

This article explores the potential benefits of commitment pacing, introduces key features and risks of drawdown and evergreen fund structures, and discusses approaches to building private equity portfolios.

Understanding Commitment Pacing and Vintage Diversification

Financial advisors can look to strategies tested by institutional investors when thinking about private equity allocations. One approach consists of pacing commitments anchored in fund vintage diversification.

Commitment pacing is an investment approach focused on the timing of capital commitments to private market funds to optimize performance and manage exposures. Commitment pacing may be enhanced through probabilistic forecasting and scenario analysis, which can better depict cash flows, net asset value forecasts, and commitment schedules. The approach is designed to support the implementation and maintenance of target allocations.2

A fund’s vintage year—the year of its first investment—can be critical because market conditions and company valuations can vary widely over time, directly influencing fund performance. For instance, funds deployed a few years apart during the dot-com bubble period showed notable differences in outcomes, with vintages from 1998 to 2000 underperforming those from 2001 to 2003.3

A structured, programmatic approach—in other words, a plan for deploying allocations over time—helps diversify private equity allocations across fund vintages, which may potentially improve capital call management and create a self-sustaining cycle for capital reinvestment. By allocating to multiple private equity funds with scaling vintages, advisors can successively use distributed proceeds to fund younger vintages when those funds call capital.

Lifecycle of Private Equity Funds

Private equity funds have variable life spans but can last around a decade, depending on the pace of fundraising, deployment, and investment exits.4

Fundraising Period: During this phase, private equity managers (general partners or GPs) secure capital commitments from investors.

Investing Period: GPs seek investment opportunities, calling capital from limited partners (LPs) once they identify targets. During this phase, GPs prove their skill by working on value creation in portfolio companies.

Harvesting Period: The fund distributes cash back to investors in the final years.

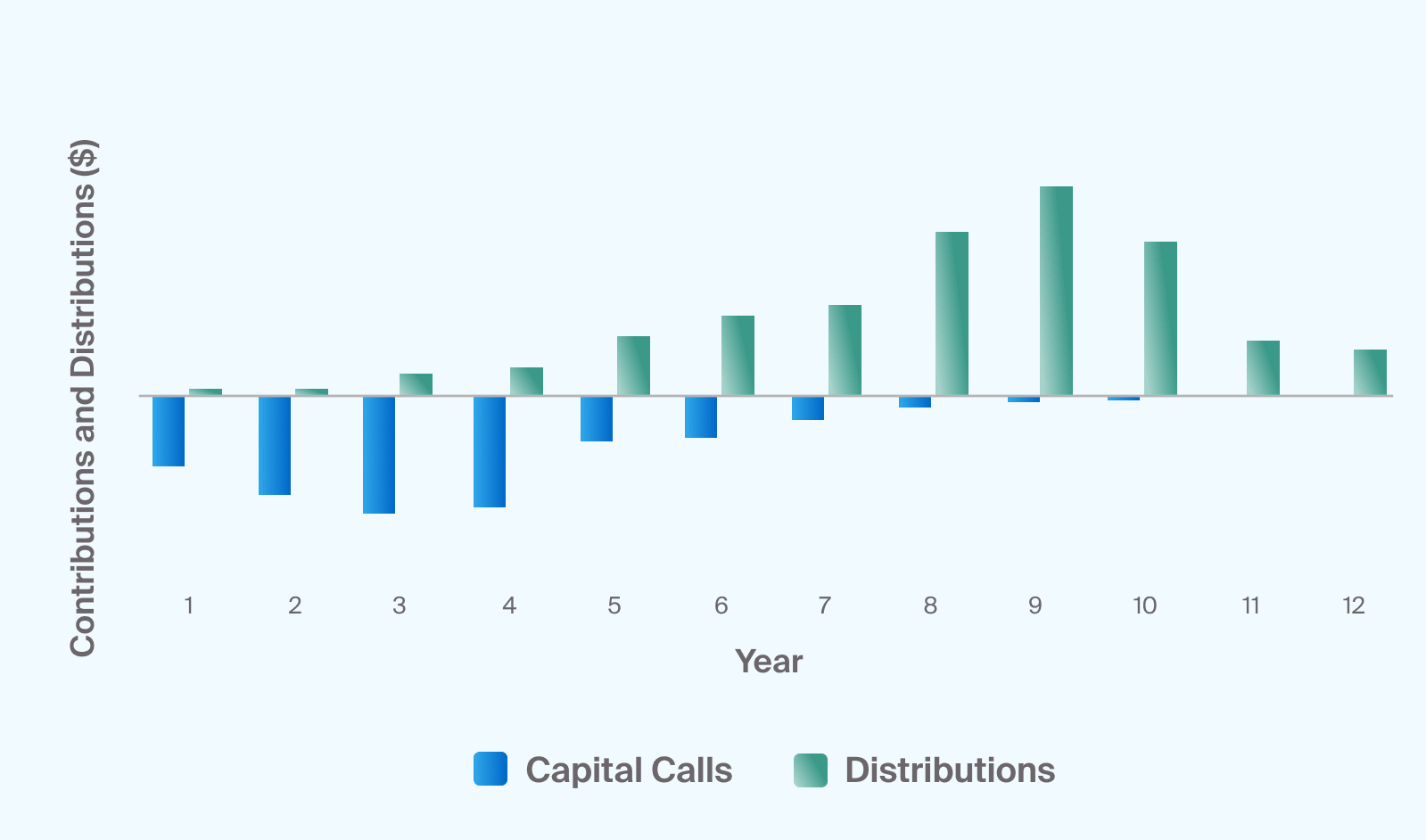

During harvesting, private equity firms often prepare for their next fund. Practicing commitment pacing can mitigate the J-curve effect. The J-curve refers to the early phase of a fund’s term when returns are typically negative, and LPs pay fees, as shown in Exhibit 1.

Footnotes

Source: Verus; For illustrative purposes only.

Commitment Pacing—Coordinated Capital Calls and Distributions: Proceeds from younger vintages can be used to fund upcoming capital calls (Exhibit 1)

While private equity managers might be working on value creation throughout the fund’s lifecycle, market conditions at the time of capital deployment, during the investment period, and at exit influence fund performance, leading to dispersion in outcomes.5

Attempting to time the market for optimal entry points often proves ineffective.6 Although past performance does not guarantee future results, understanding historical performance trends and identifying patterns across market cycles can help guide investment decisions. As highlighted in an earlier piece, when you invest can be as critical as what you invest in for achieving performance goals in private equity.

Investing in multiple vintages of a fund series, an investor can take distributions from prior funds of the same vintage program to fund commitments to the next, building a piecewise private allocation over time. A private equity allocation tied to drawdown funds requires ongoing commitments to future funds. This can help maintain the desired allocation level as committed capital gradually draws down, reducing exposure over time.

Risks Associated With Private Equity Commitment Pacing

In addition to private market investments' overarching risks, such as illiquidity, loss of capital, and use of leverage, a commitment pacing approach may introduce specific liquidity risks.

The approach inherently carries a high degree of uncertainty as it involves unpredictable factors, such as the size and timing of capital calls.

When allocations become higher than intended, especially during market volatility, risks become greater if the liquidity crunch triggers a premature sale of assets or impairs new investment opportunities.

Evergreen PE Funds

Evergreen funds, also known as perpetual funds, are designed primarily for individual investors and feature limited liquidity, according to certain conditions, such as capital availability. These funds became popular across various investor segments, amassing nearly $400 billion in assets under management as of July 31, 2024.7

These funds typically have lower investment minimums and provide immediate exposure to private equity. They generally offer monthly or quarterly investment periods and allow for gated quarterly redemptions, with fund proceeds used to meet redemption requests.

Evergreen funds come with some limitations. These include early redemption fees, redemption restrictions, and potential suspension during periods of market stress. Moreover, although these funds can attract new investors within the wealth management channel, the operational burden of managing registered funds may deter some private equity managers from developing new offerings, limiting the category’s growth.

Still, evergreen funds can be a good starting point for advisors introducing private equity to client portfolios.8 They can also complement drawdown funds, serving as a core allocation that provides limited liquidity alongside a commitment pacing program.9

Drawdown and Evergreen Funds in Core-Satellite Allocations

In public markets, capital is deployed immediately. In contrast, private markets require upfront capital commitment for deployment under uncertain market and rate conditions.

Evergreen funds may help advisors avoid the J-curve effect seen in drawdown funds, offering the potential for better early-stage performance. Drawdown funds, however, allow for strategic, layered deployments across different vintages, comprising a self-funding program aligned with the fundraising, investing, and harvesting phases of a fund’s lifecycle.10 This approach helps advisors keep allocations near their targets.

By contrast, investing in only one vintage may not capture the full performance or opportunity intended by the asset manager. To seek to reap the benefits of a vintage program, an advisor may consider investing in each vintage to mitigate concentration and to set up a potential for future self-funding.

Advisors may not need to choose between evergreen and drawdown funds exclusively. Goldman Sachs, for example, suggests that instead, they can combine both structures within a core-satellite allocation strategy. Evergreen funds, in this case, can form the core, providing diversified, multi-sector exposures to private-equity-backed companies. Drawdown funds then allow for more customized exposures to targeted sectors, geographies, or themes with potential for outperformance.11

Considerations About Commitment Pacing Programs

When structuring private equity portfolios, it is important to evaluate managers’ track records and consider factors such as:

Commitment Sizing: Estimating total asset net growth and net cash outflow can help size and pace commitments for vintage diversification.12

Future Commitments: Projecting future commitments can help advisors keep exposures while accounting for distributions earmarked for redeployment.13

Volatility Impact: Assessing short-term volatility’s impact on long-term commitments can inform capital call management and liquidity needs.14

Alternative Capital Sources: It can be important to identify potential sources of additional capital if equity markets decline or exits from drawdown funds slow down.

Performance Trends: Understanding the historical performance patterns of evergreen and drawdown funds can help an advisor meet return goals and build satellite private equity portfolios. An analysis by Goldman Sachs, assuming the same underlying private assets in evergreen and drawdown funds points to an additional 2.25-2.75% in annualized net return (time-weighted) in a drawdown structure compared to an evergreen one. Portfolio composition, fee structures and calculation method differences affect the performance of evergreen and drawdown funds. In drawdown funds all assets are invested in private holdings, while in evergreen ones, managers tend to hold some cash and lower yielding publicly traded securities, detracting from performance.15

Operational Considerations: Leveraging features of alternative investment platforms, such as integration with custodians, can alleviate operational burdens and simplify capital call management of drawdown funds.